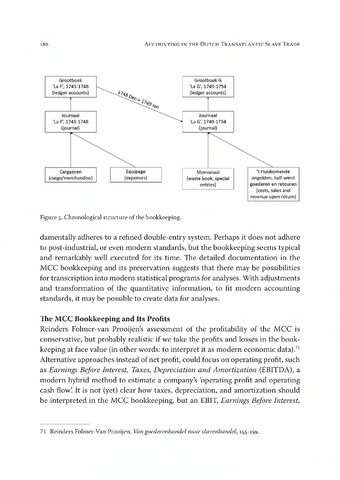

damentally adheres to a refined double-entry system. Perhaps it does not adhere

to post-industrial, or even modern standards, but the bookkeeping seems typical

and remarkably well executed for its time. The detailed documentation in the

MCC bookkeeping and its preservation suggests that there may be possibilities

for transcription into modern statistical programs for analyses. With adjustments

and transformation of the quantitative information, to fit modern accounting

standards, it may be possible to create data for analyses.

The MCC Bookkeeping and Its Profits

Reinders Folmer-van Prooijen's assessment of the profitability of the MCC is

conservative, but probably realistic if we take the profits and losses in the book

keeping at face value (in other words: to interpret it as modern economic data).71

Alternative approaches instead of net profit, could focus on operating profit, such

as Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA), a

modern hybrid method to estimate a company's 'operating profit and operating

cash flow'. It is not (yet) clear how taxes, depreciation, and amortization should

be interpreted in the MCC bookkeeping, but an EBIT, Earnings Before Interest,

186

Accounting in the Dutch Transatlantic Slave Trade

Cargazoen

(cargo/merchandise)

Equipage

(expenses)

Grootboek G

'La G', 1749-1754

(ledger accounts)

Journaal

'La G', 1749-1754

(journal)

Grootboek

'La F', 1743-1748

(ledger accounts)

Journaal

'La F', 1743-1748

(journal)

Memoriaal

(waste book, special

entries)

't Huiskomende

ongelden, half-winst

goederen en retouren

(costs, sales and

revenue upon return)

Figure 5. Chronological structure of the bookkeeping.

71 Reinders Folmer-Van Prooijen, Van goederenhandel naar slavenhandel, 155-159.

{kind=link}